Subscription Churn Analysis: Finding and Fixing Revenue Leaks

Every subscription business leaks revenue. Some leaks are obvious: a spike in cancellations after a price change, a batch of failed credit cards. Others are slow and quiet, a gradual decline in retention from one acquisition channel, or a creeping uptick in pauses that precede full cancellations by a few weeks.

Churn analysis is the discipline of finding those leaks, understanding what causes them, and fixing them in order. This guide is the framework we use, drawn from eleven years of running subscription retention at Scentbird and now packaging that work at Finsi.

Understanding subscription churn

Subscription churn rate is the percentage of subscribers who cancel or fail to renew within a given period. The monthly formula:

Monthly Churn Rate = (Subscribers Lost During Month / Subscribers at Start of Month) x 100

5% monthly churn does not sound alarming. Compounded across a year, you lose nearly 46% of your base. Small improvements in monthly churn have an outsized impact on annual revenue and on valuation.

Subscription businesses are valued on retention. A business at 3% monthly churn is worth dramatically more than the same business at 6%, even with identical current revenue. The lifetime value gap cascades through every line in the model.

Voluntary vs. involuntary churn

The first split in churn analysis is voluntary versus involuntary. They have different causes, different fixes, and different difficulty levels. Confusing them is the most common mistake we see.

Voluntary churn

Voluntary churn happens when a customer makes a conscious decision to cancel. The common drivers:

Perceived value erosion. The customer no longer feels the subscription is worth the price. Product quality declined, their needs changed, or a competitor looks better.

Product accumulation. Common in physical-product subscriptions: the customer has more product than they can use and feels wasteful continuing to receive shipments.

Financial pressure. The customer is cutting discretionary spending and your subscription does not survive the cut. Often seasonal or correlated with broader economic conditions.

Experience friction. Poor customer service, shipping problems, website issues that make the subscription feel like a hassle.

Buyer's remorse or impulse signup. The customer signed up during a promotion or a moment of enthusiasm and never built a real habit around the product.

Involuntary churn

Involuntary churn happens when the subscription ends due to payment failure, without the customer choosing to cancel. Common causes:

Expired credit cards. The most common cause. Cards expire on a regular cycle, and unless the customer updates the payment information, the next charge fails.

Insufficient funds. The charge hits when the account is short. This can be timing (charge before payday) or genuine constraints.

Card issuer declines. Banks decline charges for fraud flags, spending limits, or other risk signals, even when the customer fully intends to keep paying.

Account closures. The customer closed or replaced the bank account or card, often without remembering every subscription tied to the old one.

For most subscription businesses, involuntary churn is 20-40% of total churn. Because these customers did not choose to leave, recovery potential is high, and addressing involuntary churn is almost always the fastest path to lower overall churn.

Cohort analysis

Cohort analysis is the backbone of churn work. By grouping subscribers by signup month and tracking retention over time, you see patterns the aggregate completely hides.

Building the analysis

- Group subscribers by signup month. Each monthly cohort starts at 100%.

- Track the percentage remaining at each subsequent month. Month 1, month 2, through month 12 and beyond.

- Plot retention curves for each cohort. The visual makes the trends jump out.

What to look for

Early-stage churn patterns. Most subscription businesses see their highest churn in months one through three, when uncommitted subscribers leave. If month-one churn is well above benchmark (10-12%), your acquisition is bringing in low-intent subscribers, your onboarding is weak, or both.

Steady-state churn. After the early-churn period, monthly churn should stabilize. Where it stabilizes is one of the most important numbers in your business. It determines long-term subscriber economics.

Cohort comparison. Are newer cohorts retaining better or worse than older ones? Improving cohort retention means your product or experience changes are working. Declining cohort retention is an urgent warning.

Seasonal patterns. Some months produce systematically different retention. January cohorts often include resolution signups that churn fast. Holiday cohorts include gift subscriptions with limited natural lifespans.

Segmenting your churn data

Beyond cohorts, segmenting churn reveals which customers are most and least likely to leave.

By acquisition channel

Different channels attract different profiles with different retention curves. Look at churn rate by source:

- Organic search subscribers retain differently than social-acquired ones

- Referrals tend to show the strongest retention

- Heavy promotional offers attract deal-seekers with higher churn

- Influencer-driven signups often start enthusiastic but vary widely on long-term retention

This should feed directly into your acquisition strategy and your LTV:CAC math by channel.

By plan or product

If you have multiple tiers, churn rates will differ. A premium tier often retains better than a basic tier, suggesting customers who invest more are more committed. A specific product with elevated churn usually points to a quality or fit problem.

By customer behavior

Behavioral segments catch what demographic and acquisition segments miss. At Scentbird we saw subscribers who engaged with content or community in their first month retain at roughly twice the rate of those who did not. Subscribers who customized their first box also retained better than those who took the default.

Behavioral signals point straight at interventions. If community engagement correlates with retention, investing in community building is a retention move, not just a brand exercise.

By cancellation reason

The most directly actionable segmentation, but only if you capture cancellation reasons well.

Cancellation reason capture

When a subscriber cancels, capture why. The quality of that data depends entirely on how you collect it.

Building the survey

Required but short. One question, pre-defined options, and a free-text field. Do not make customers jump through hoops to cancel. It creates resentment and eventually attracts regulators.

Specific, actionable categories. "I'm not satisfied" is too vague to use. Better:

- "I have too much product / can't use it fast enough"

- "The product isn't right for me / my needs changed"

- "It's too expensive for my budget right now"

- "I found an alternative I prefer"

- "I had a problem with shipping or delivery"

- "I didn't like the product selection or variety"

- "I only meant to order once / signed up by mistake"

Free-text field. Pre-defined options capture the broad buckets, free-text catches specific fixable issues you would never have thought to list.

Analyzing the data

Track cancellation reasons over time, not just in aggregate. A spike in "too expensive" after a price change is immediate feedback. A gradual rise in "found an alternative" signals competitive pressure that needs a strategic response.

Cross-reference reasons with subscriber characteristics. If "too much product" dominates among monthly subscribers but rarely shows up among bi-monthly ones, the fix is promoting plan flexibility, not changing the product.

Dunning optimization

Dunning, the process of recovering failed payments, is the most cost-effective churn reduction lever for most subscription businesses. Every recovered payment is a saved subscriber with no discount, no incentive, no intervention cost.

Pre-dunning: prevent failures

Card expiration alerts. Email and SMS at 30, 14, and 3 days before a card on file expires, with a one-tap link to update. This single tactic prevents a meaningful chunk of involuntary churn.

Account updater services. Most payment processors offer an automatic card updater that refreshes expired details without customer action. The lowest-friction solution available. Turn it on if your processor supports it.

Active dunning: recover failed payments

Smart retry logic. Not every failure should be retried immediately. The right retry depends on the failure reason:

- Insufficient funds: retry a few days later, ideally aligned with common pay cycle dates (1st, 15th)

- Temporary processor issues: retry within hours

- Hard declines (closed account, stolen card): do not retry, contact the customer directly

Escalating communication. When a payment fails, run a sequence:

- Immediate notification. A simple, non-alarming email letting them know the charge did not go through with a one-click link to update the payment method.

- Reminder at 3-5 days. Follow up if the payment is still unresolved, emphasizing the subscription is at risk.

- Final notice at 7-10 days. Clear message that the subscription will be paused or cancelled if payment is not resolved, with an easy resolution path.

- SMS follow-up. If email gets no response, SMS cuts through inbox noise.

Optimized timing. Test time of day and day of week for both retries and dunning emails. Retries on payroll-aligned days have higher success rates. Dunning emails sent at certain times pull better open and action rates.

Measuring dunning

The metrics that matter:

- Initial payment failure rate: percentage of charge attempts that fail

- Recovery rate: percentage of failed payments eventually recovered

- Time to recovery: average days to recover a failed payment

- Recovery by method: automatic retry vs. customer action

- Final churn rate from failed payments: percentage of failures that ultimately cost you the subscriber

A well-run dunning process recovers 50-70% of failed payments. If you are below 40%, there is real room to improve.

Pause and downgrade alternatives

Giving subscribers an alternative to outright cancellation is one of the highest-impact voluntary churn levers we have used.

Pause

Let subscribers pause for a defined period (one to three months). A subscriber who pauses is far more likely to come back than one who cancels and has to go through signup again.

Track pause conversion rate (would-be cancellers who pause instead), resume rate (paused subscribers who reactivate), and time to resume. If pause-to-resume is above 50%, the option is saving real subscribers.

Downgrade

If you have multiple tiers, offering a downgrade in the cancellation flow saves subscribers whose primary objection is price. A subscriber who moves from $49/month to $29/month is still revenue and still in your ecosystem.

Frequency adjustments

For product subscriptions, switching from monthly to bi-monthly or quarterly addresses the "too much product" reason without losing the subscriber.

Product swap or customization

Allowing subscribers to change what they receive addresses "I didn't like the selection" cancellations. The more control they feel they have, the less likely they are to cancel.

Building a churn prevention program

Effective churn work is not a collection of one-off tactics. It is a program with defined processes, metrics, and ownership.

Step 1: establish baselines

Before improving churn, know exactly where you stand. Calculate monthly churn split by voluntary and involuntary. Build cohort retention curves for the last 12 months. Categorize cancellation reasons. Calculate current dunning recovery rate.

Step 2: fix involuntary churn first

Almost always the quickest win. Implement card expiration alerts, optimize retry logic, build a dunning email sequence, enable account updater services. These changes typically cut involuntary churn 30-50% with relatively little engineering effort.

Step 3: add cancellation alternatives

Pause, downgrade, and frequency adjustment in the cancellation flow. Track save rate per option and tune based on which alternatives work best for which reasons.

Step 4: build early warning

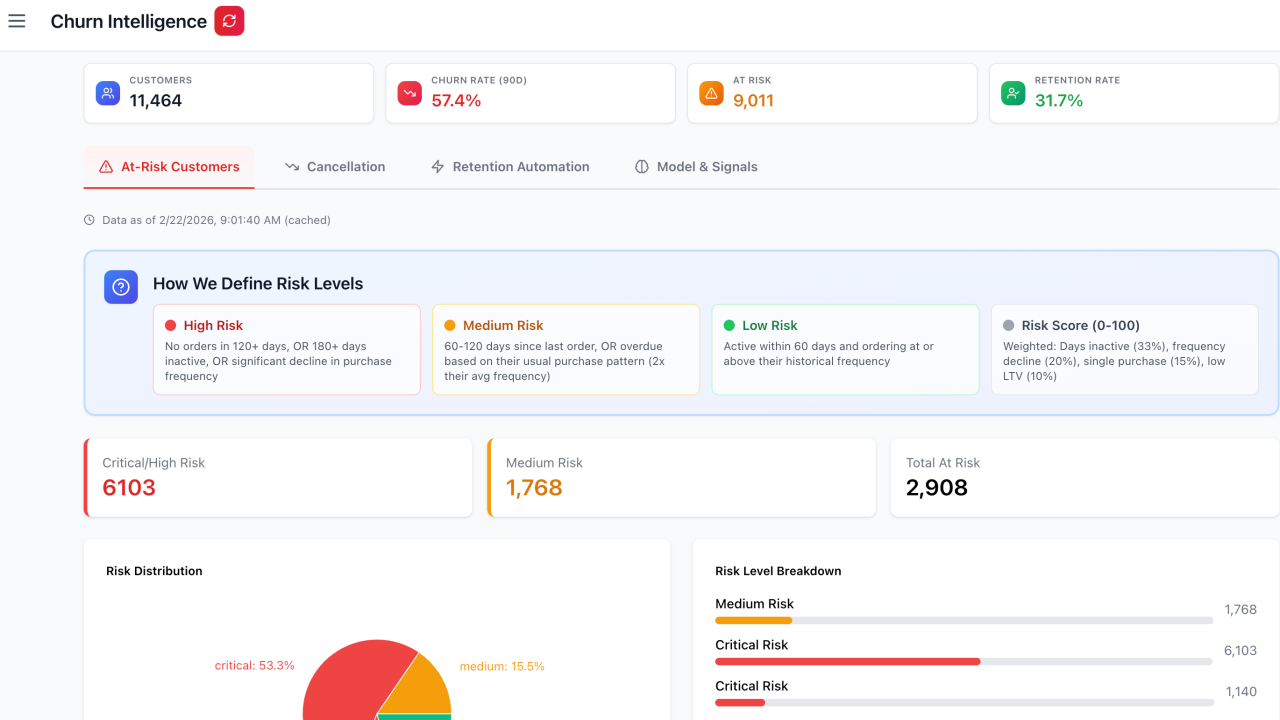

Engagement data, behavioral signals, and predictive models surface at-risk subscribers before they hit the cancellation page. Finsi's retention intelligence scores churn risk automatically and flags subscribers showing disengagement patterns.

Intervene early. A check-in email, a product recommendation, an invitation to give feedback. The earlier you engage with an at-risk subscriber, the better the odds of saving them.

Step 5: segment-specific retention plays

Different segments churn for different reasons and respond to different interventions. Build playbooks for the segments that matter most:

- New subscribers (months 1-3): onboarding, product education, habit formation

- Mid-tenure (months 4-12): value reinforcement, variety, community

- Long-term (12+ months): recognition, VIP treatment, deepening the relationship

- Price-sensitive churners: downgrades or promotional pricing

- Product-dissatisfied churners: swaps, customization, direct feedback channels

Step 6: win-back

Some churn is unavoidable. But cancelled subscribers are far easier to reactivate than entirely new customers. They already know the brand and have made the buying decision once before.

Build a structured win-back sequence that fires shortly after cancellation, with relevant offers based on the cancellation reason:

- Cancelled on price: discounted rate or smaller plan

- Cancelled on accumulation: less frequent plan

- Cancelled on dissatisfaction: come back after the underlying issue is fixed, with a specific message about what changed

Track win-back conversion by reason and by time since cancellation. Most success happens in the first 30-60 days. After 90 days the probability drops sharply.

Step 7: measure, learn, iterate

Churn prevention is ongoing. Establish a regular cadence:

- Weekly: overall churn rate and dunning recovery rate, looking for sudden changes

- Monthly: cohort retention trends, cancellation reason distribution, intervention effectiveness

- Quarterly: deep analysis by segment, channel, and product, then update playbooks

Modeling the revenue impact

To get organizational buy-in for churn investment, quantify the upside.

A simple model. 10,000 subscribers paying $40/month at 6% monthly churn loses about 600 subscribers a month, or $24,000 in MRR. Over a year that compounds into a serious drag on growth.

Drop monthly churn from 6% to 5%, a single point of improvement, and you retain an additional 100 subscribers per month. After 12 months, that compounds to roughly 780 additional active subscribers, $31,200 in additional MRR, and $374,400 in additional annual revenue. That math beats virtually any churn prevention budget.

Wrapping up

Subscription churn is a solvable problem if you treat it as a discipline. The brands that hit best-in-class retention treat churn prevention as a core business function rather than something the retention team handles in spare time.

Start by understanding your churn composition: how much is voluntary versus involuntary, which cohorts and segments are most affected, what reasons drive cancellations. Fix involuntary churn first for the quickest wins. Then build toward proactive, predictive approaches that catch at-risk subscribers before they reach the cancellation page. That is a big part of why we built Finsi.

The gap between 5% and 3% monthly churn sounds small. Over 12 to 24 months it compounds into a fundamentally different business.

Stop guessing. Start knowing.

Finsi connects your e-commerce data, tells you what to do, and executes it: email campaigns, ad optimization, retention flows. Free 30-day trial.